UP RERA REGISTRATION PROCESS

Real Estate Regulatory Authority (RERA), since its inception in 2016 has been working towards creating more equitable and fair transactions between the seller and the buyer of properties. RERA has been making real estate purchases easier with increased accountability, transparency and also by providing increased incentives for new projects.

One of the primary reasons for delayed, incomplete projects was funds of one project being diverted to funds for some new project. To work out a solution for the same, under section 4 (2) (1) (D) of the RERA Act, 2016 it is provided that seventy percent of all the account that a builder receives from the allottees must be deposited in a separate bank account to cover the cost of construction of the project. It is also provided in the provisions that the amount that could be withdrawn from such a bank account would be in proportion to the percentage of completion of the project. Moreover, the amount could only be withdrawn after it is certified by an engineer, an architect, and a chartered accountant in practice.

But despite various directions, it has been found that these provisions were not being followed. In many cases correct account details were not being provided and, in some cases, the same bank account has been registered for more than one project which violates the provisions of the law. In some other cases, there are complaints of how there were no bank accounts to start with, or the money submitted in these accounts is being used for an expense not related to the project. Considering all the loopholes in the provisions that were being exploited, UP-RERA rolled out revised directions in December 2020 to manage the shortfalls of the original provisions. This article aims to explain these revised directions and to make the process of registering a project with UP-RERA easier.

Please feel free to contact the undersigned if you need any clarification for the same.Or you are looking RERA Consultant Delhi or UP RERA Consultant

-

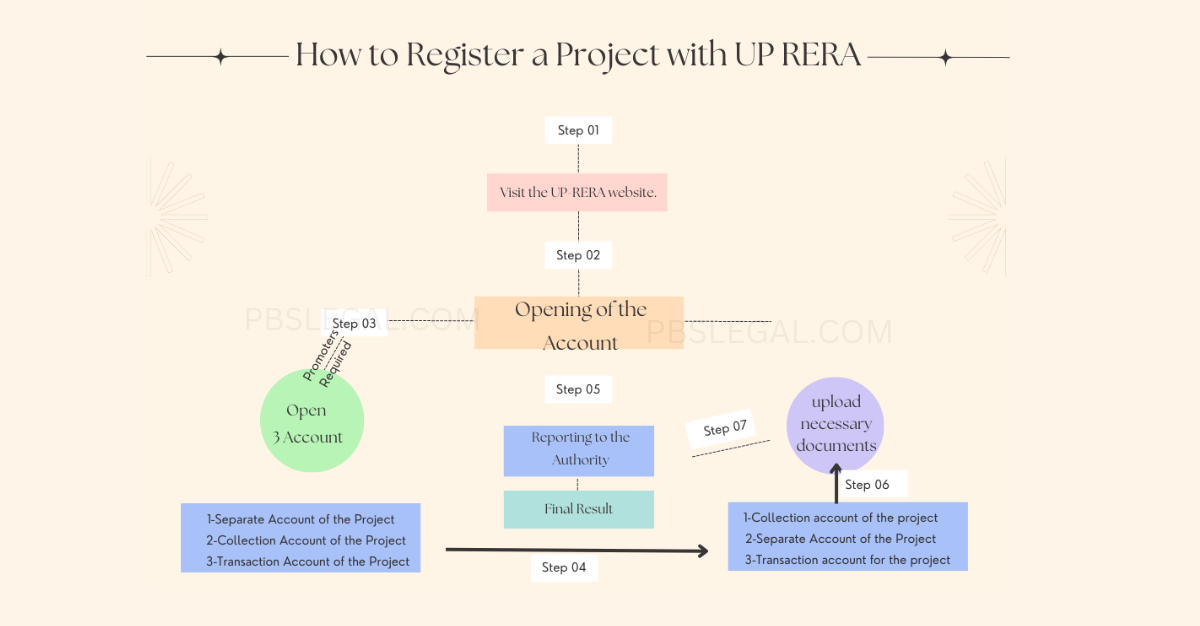

Opening of the Account

The promoter is now required to open three accounts.

- Separate Account of the Project

- Collection Account of the Project

- Transaction Account of the Project

These three accounts must be opened before a promoter applies for registration in UP-RERA and all the details of these accounts shall be submitted along with the application of registration. All the three accounts and their application are discussed below” –

-

Collection account of the project

A collection account shall be opened for each project separately. UP-RERA is quite specific with regards to the directions and even goes to provide how a bank account shall be named. For example – if the name of the promoter is M/s ABC Ltd, and the name of the project is XYZ, then the description of the account will be “ABC – Collection Account for XYZ”.

Collection account is the account where the promoter shall be depositing the collections received from the allottees including the GST. The promoter shall give instructions to the bank to auto-transfer not less than seventy percent of the total amount, excluding the GST in the ‘Separate Bank Account of the Project’ and not more than thirty percent in the ‘Transaction Account of the Project’.

-

Separate Account of the Project

Separate bank accounts for each project are mandatory. The bank account shall have the <name of the project> along with the name of the holder of the Separate Bank Account of the Project. For example, if the name of the promoter is M/s ABC Ltd, and the name of the project is XYZ, then the name of the account should reflect as “ABC – Separate Bank Account for XYZ”.

As stated earlier, seventy percent of the amount in the Collection Account must be deposit here and this seventy percent ratio must be maintained throughout the project development. The loan taken up to finance the project whether secured or not must also be deposited in this account. Furthermore, if any amount needs to be withdrawn from this account the certificates by practicing architect, engineer, and chartered accountant is required. One important requirement to keep in mind is that the chartered accountant issuing this certificate shall be an entity other than the statutory auditor of the promoter. The amount withdrawn however can’t be used for paying off the penalties, interest, or compensations by the promoter.

The promoter can utilize the money from this account for repayment of interest payable on account of the project finance. It shall be done at the same rate of interest which the bank or the FI (Financial Institution) or the NBFC (Non-Bank Financial Companies) is charging. The same is also applicable for unsecured loans. UP-RERA advises the promoter to not use the amount in the Separate Account of the project for day-to-day transactions.

-

Transaction account for the project

Like all other two accounts, a separate account is mandatory for each project. If the name of the promoter is M/s ABC Ltd, and the name of the project is KYZ, then the name of the account should reflect as “ABC – RERA Transaction Account for XYZ”. A maximum of thirty percent of the total amount of the Collection Account can be submitted in the Transaction Account. This account can be used to cover expenses that are not directly related to the construction of the project, for example: – refund to the allottees, penalties, interest, and compensations.

Once in existence, the promoter has to disclose the three accounts to UP-RERA through its website. The promoter is expected to submit the copies of the passbook/ latest bank statement of all three accounts of the project along with the affidavit (RA-1) available inside the notice titled, “Real Estate Project (Maintenance and Operation of Separate Bank Account) Revised Directions, available on the UP-RERA website along with the application for registration of the project. All necessary contractual and legal arrangements for operating the account must be submitted if there is more than one promoter of the project.

Reporting to the Authority

All the withdrawals and collections in these three accounts must be reported to UP-RERA regularly. After six months of the end of every financial year, the promoter must get all the accounts audited by a chartered accountant. It shall be certified by such chartered accountant that the amount withdrawn from the accounts was for the development of the project and was in proportion to the ratio mentioned above. This entire statement must be uploaded on the UP-RERA website.

Another important factor to note is that if the authority finds out that the statement uploaded on the website by the architect, engineer, and the chartered accountant is false or is not in compliance with the guidelines of the act, then the authority is equipped to take penal action against such individual and would also take up the matter with the concerned regulatory authority of the professional for penal action against them.

The promoter shall submit the details of any project finance availed for the project at the end of every quarter using the online facility on the website of the authority.

This is the process through which a promoter should register their projects with UP-RERA. All the certificates mentioned in the article above are available on the UP-RERA website inside the notice titled, “Real Estate Project (Maintenance and Operation of Separate Bank Account), Revised Directions”.

Reference:https://www.up-rera.in/pdf/Documents.PDF

{kind=link}

{kind=link}

Leave A Comment